What are the lessons learned by Microfinance Organizations from COVID-19 pandemic? We share the results of a study conducted by our group organization, Belstar Microfinance across its customer base. This study also helped Belstar prepare itself for a post-COVID world.

With the COVID1-19 pandemic, lives and livelihoods across the nation were affected and the economically weaker section witnessed a huge blow. Workplaces shut down, bringing millions of workers and small business owners among others to deal with the loss of employment, fall in income levels, food shortages and uncertainty about their future.

To build a deeper understanding of the livelihood crisis especially within its customer base, and explore solutions to address some of the existing customer level challenges, Belstar Microfinance Limited (Belstar) and Hand in Hand, India, undertook an impact study.

A Study on the Impact of COVID-19 in Rural India

The study was undertaken in all 17 states and Union territories that Belstar has its microfinance operations. The respondents were selected through a purposive sampling method to ensure diversity in location and type of work done. An average of 100 regular customers per state, with payment/non-payment records in the month of May was chosen. More than 90% of the survey sample belonged to rural areas. The respondents were interviewed between June 15 and June 30, 2020; thus, the findings might differ with respect to the current circumstances.

The Objective of the study were two:

– Understand the extent of impact on livelihood on their existing clients

– Understand the financial health of the customer base

Key Findings

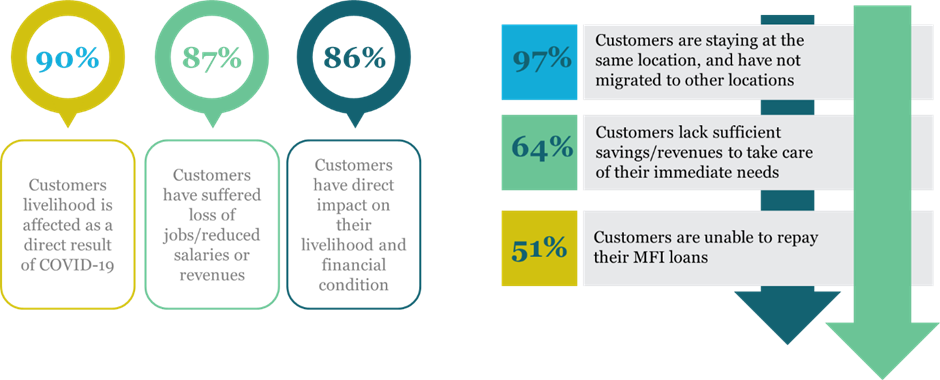

1. Almost 90% livelihood of the customer base are affected as a direct result of COVID-19

While the effect on livelihood impact of Covid-19 was well known, it has massively hit the customer base of microfinance institutions (MFIs).

89.8% of the respondents reported that they have been affected by the aftermaths of the Covid-19 virus. This is primarily because the microfinance companies cater to third quintiles of the income distribution pyramid and have very minimal stability of income.

Odisha and West Bengal had a double whammy hit of Covid-19 and cyclone Amphan during the said period, which resulted in 100% affect to the customer base during the lockdown period.

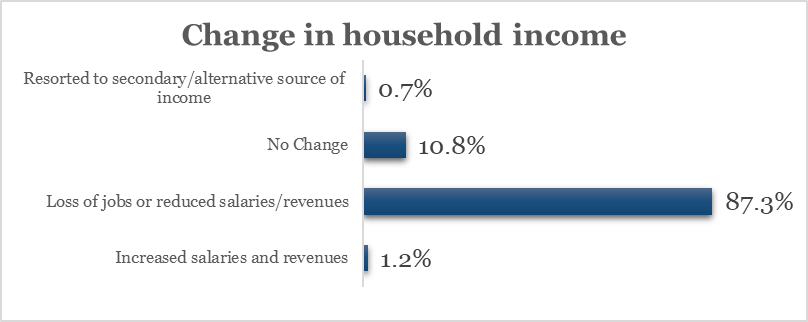

2. Job loss for 87% of customers

More than 87% of the customers contacted have either lost their job or must live with reduced salary/revenues. Merely 12% of the customer base reported either No change or increase in revenue, during the lockdown period.

A similar macro level study conducted by Rustandy Centre for Social Innovation, has also reported 84% of households had a fall in income, due to the lockdown.

Movement restrictions played a pivotal role in hampering the livelihood of the customers. States like Gujarat and Kerala where there was an initial outburst of Covid-19, the livelihood got impacted because of concerns of leaving household (due to health) and limited transport facility. Furthermore, the impact was worsened by reduction in demand and inaccessibility to markets.

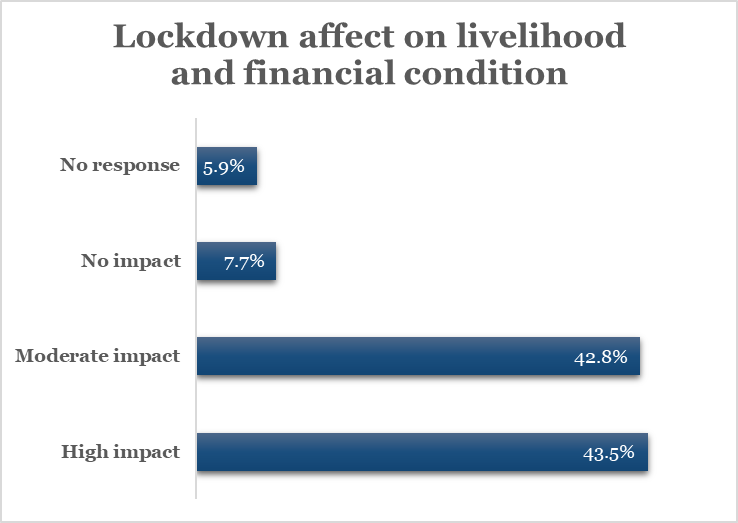

3. Livelihood impact on customers

The spread of the epidemic and the economic lockdown enacted in response have impacted the daily lives of nearly all Indians. The same has been certified by respondents interviewed, who felt the heat of the lockdown in their livelihood and financial conditions.

More than 86% customers have been impacted as per the survey. The customer base comes from a section with predominantly labours and working-class population, who are more prone to income fluctuations. Various studies validate this assessment, for a similar customer segment.

4. Lack of immediate savings for 64% customers

More than 85% respondents have a family of 4 or more. Given the low baseline wealth of many households, a large share of Indian households’ state that they will be unable to continue — even over relatively short periods — without additional assistance. Across India, 64 percent of all households’ report being unable to survive without additional assistance.

5. More than half the customers are unable to repay their MFI loans

The severe effects on the livelihood of the people are likely to impact their capability to continue loan repayments of microcredit lending institutions. Around 40% respondents have an exposure to more than 1 MFI while 86% have an average total loan outstanding between Rs. 25,000 – 50,000

Despite high number of households reporting low in savings, a good 49% of clients have shown willingness and stability to repay their MFI loans. This can be attributed to the microfinance sector which is unique in being a double bottom line of financial and social objectives. The sector has stood with its customers in tough times, and the customer has also shown resilience time and again.

6. Little or no migration to other locations

Though problems with migration of labor, and its aftermath have caught many eye balls in the country. As per our data assessment, only 3% of the surveyed client base has relocated with states like West Bengal, Uttar Pradesh, Maharashtra, and Gujarat reporting 0% migration issues.

However, for the ones staying at the same location, sustaining their household needs is a bigger challenge. In such a crisis, sensitivity of lending institutions towards their economic welfare will instil a sense of trust and belongingness among the borrowers, thus assuring lesser payment defaults in future.

However, for the ones staying at the same location, sustaining their household needs is a bigger challenge. In such a crisis, sensitivity of lending institutions towards their economic welfare will instil a sense of trust and belongingness among the borrowers, thus assuring lesser payment defaults in future.

The Assessment

The COVID-19 pandemic and the consequent lockdown infused a sense of fear for both health security and financial stability. The effect was acutely felt by the lower stratum of the financial pyramid who are already prone to financial instability. While the disruptions in livelihood have been severe, the chances of reviving a steady income have also dwindled, given the fragile state of economy.

The analysis revealed two important conclusions:

• Due to impact on livelihood, a large majority of the customer base is having a Saving crisis at their household

• Customers with higher loan outstanding range have a high probability to default/delay the loan repayment to MFIs

Also, the Financial Stability Report of RBI states that the overall economy is going through a tough time and the proportion of NPAs with the banks are likely to go up. As per the report, ‘Macro stress tests for credit risk indicate that the GNPA ratio of all SCBs may increase from 8.5 per cent in March 2020 to 12.5 per cent by March 2021 under the baseline scenario. If the macroeconomic environment worsens further, the ratio may escalate to 14.7 per cent under very severe stress.’ This leads us to an estimated increase in NPAs for MFIs in a substantial manner.

The above estimates lead NBFC-MFIs to a vicious cycle of increased payment defaults and reduced operational sustainability, which furthers increases the difficulty in arranging for bank funds to sustain their operations. The risks further strengthen for institutions with smaller sized Balance sheets.

Interventions

Preparedness to deal with potential NPAs

While the collections within microfinance sector is slowly gaining momentum, we estimate 5-10% of the current loans to turn NPAs . Subsequently, as the economists don’t expect a V-shape recovery, augmenting capital, reducing operating expenses, and creating upfront provisions can help balance the expected rise in PAR.

Focal shift from expansion to stability

MFIs are likely to become risk averse and would not target new client onboarding and fresh geographies. The business expansion must be gradual and cautious, focusing more on quality of the disbursements instead of being aggressive. The state-wise difference in severity of impact on livelihood, can help assess expansion potentiality and reduce negative repercussions.

Innovative but customer centric business approaches

While this lockdown has been a jolt to the MFIs, it has also opened arenas for adopting long pending innovative techniques. MFIs can harness technology to keep their clients connected to the financial system even in the face of crisis. The use of technology mitigates the risk and lack of information associated with underserved households via digital financial services and enhanced risk-assessment skills.

In such testing times, it is important for MFIs to retain their customers and its goodwill in the market, apart from gradually recuperating its business operations. The need of the hour is to evaluate the effect of pandemic and lockdown on the customer base and estimate the impending impression of this effect on business activities, thus enabling the management to make informed decisions. At the same time, it gives us an opportunity to assure the customers that apart from being a lending entity, the organization is also committed to ensure the greater good of its clients.

This study was authored by Divyani Jain, Biju Sasidharan and Arpan Sahni of Belstar.

Belstar Microfinance Limited (Belstar) is a Non-Banking Finance Company (NBFC) and a subsidiary of Muthoot Finance Limited. Belstar’s business model is unique as it pursues a double bottom line focusing on both financial performance as well as social performance with the assistance of the Hand in Hand India in alleviating poverty coupled with community development. Belstar provides microfinance loans in semi-urban and rural areas under the SHG and JLG-based lending models.

As on March 31, 2020, Belstar operates in 17 states and one Union Territory with 603 branches and a loan portfolio of INR 2630 crore and 12 lakh borrowers.

If loans were granted and utilised for a Economic Activity or the loaner is already undertaking a Economic Activity generation of income and repayment may not be a problem. Now onwards, flow of credit towards persuing economic activity may be encouraged so that repayment risk may be mitigated. This is my experience while lending to SHG’s and promoted and encouraged some economic activities by the SHG members and recovery rate was above 98% and loaners also well placed in the society.